Are Crypto Trading Bots Profitable? The Fee Math That Decides

Most bots don't fail because the strategy is bad. They fail because trading fees eat an edge that was only a few basis points wide to begin with. Here is the math, and the 3 ways to shift it.

- A bot's edge per trade is usually measured in basis points, and a taker round trip on futures costs 10 to 12 of them. Whether a bot is profitable is decided in that gap.

- Bots pay exactly the same maker and taker fees as manual trading. There is no separate API fee schedule on Binance, Bybit or any major exchange.

- Exchange choice for bots comes down to 3 things: API infrastructure, depth of liquidity, and the effective fee after discounts. Most builders only compare the first one.

- Arbitrage and grid bots are the most fee sensitive strategies; a fee change of 2 basis points can flip their whole backtest from green to red.

- Fee cashback works with API trading out of the box: it runs on the account UID, so 30 to 50% of the fees a bot generates come back without touching a line of its code.

Backtests love to skip the unglamorous line items. Slippage gets a parameter, fees get a footnote, and then a strategy that printed money on paper bleeds out in production at 2 trades per hour. The truth about bot profitability is mostly arithmetic, and the arithmetic is dominated by trading fees. This guide runs the numbers a bot actually faces on a real exchange, then shows where the fee line can be moved.

The math: edge per trade vs fee per round trip

A bot is profitable when its average edge per trade is larger than its average cost per trade, and for most bots the dominant cost is the fee.

The numbers are small and unforgiving. On USDT perpetuals, standard taker fees sit between 0.050% and 0.060% on the major venues, so one round trip, open plus close, costs 10 to 12 basis points as a taker. A grid bot taking profits on 0.4% steps gives a quarter of every winning step back in fees at those rates. A strategy with a genuine 15 basis point average edge keeps just 3 to 5 of them after taker fees, and a single losing streak swallows the rest.

The same strategy filled as a maker pays 4 basis points per round trip and keeps 11. That difference, 7 basis points per trade, compounds across thousands of trades into the entire distance between a dead bot and a live one. Run this calculation before any backtest: average edge per trade in basis points, minus fee per round trip at the rates you will actually pay.

What API trading really costs

Orders placed over the API pay exactly the same maker and taker rates as orders clicked in the UI. There is no separate API fee.

The schedules published by Binance, Bybit and OKX apply to every order regardless of how it reaches the matching engine. What does differ per exchange is everything around the order: rate limits decide how fast a bot can quote and cancel, weight systems decide how many requests it can spend per minute, and colocation or websocket quality decides how stale its view of the book is. Those constraints shape which strategies are even feasible.

But on the cost side, the only numbers that matter are the same maker and taker percentages every other trader pays, which means every fee discount available to a human applies to a bot too.

Choosing an exchange for a bot: the 3 things that matter

Infrastructure, liquidity, fees. In that order of attention for most builders, and roughly the reverse order of what shows up in the monthly result.

API infrastructure sets the floor: uptime, websocket stability, sane rate limits and predictable error handling decide whether the bot runs at all. Depth of liquidity decides the real execution price; on a thin book, slippage can quietly cost more than fees, and a backtest on top of book data will not show it.

The effective fee then decides what survives of the edge, and effective is the operative word: the printed schedule minus VIP tier, minus token discount, minus cashback. Two exchanges with identical headline fees can be 30 or 40% apart in effective cost once discounts are applied. A bot that turns over serious volume should be placed where the deepest book and the lowest effective fee meet, and that comparison has to be run with real numbers, not the marketing page.

Which strategies are most fee sensitive

The higher the trade frequency and the thinner the per trade edge, the more the fee decides the outcome.

Cross exchange arbitrage sits at the extreme: the spread being arbitraged is often smaller than 2 taker fees, which is why serious arbitrage desks obsess over fee tiers before they obsess over latency. Grid and DCA bots come next; they trade constantly and bank many small wins, so the fee share of each win is structurally high. Market making lives entirely on the maker rebate side of the schedule and is not viable at standard taker rates at all.

Trend following and swing bots sit at the relaxed end, with fewer, larger trades where 10 basis points hurt but rarely decide the year. The practical rule: the more your bot's equity curve looks like a staircase of small steps, the more of that staircase is built on the fee line.

Are AI trading bots any more profitable?

AI trading bots change how signals are generated, not what a trade costs. Whether the entry comes from a grid rule, a momentum model or an LLM reading sentiment, the exchange charges the same taker fee on the same notional, and the fee drag math in this article applies unchanged.

The honest read on the current AI-bot wave: better models can raise the hit rate, but they also tend to trade more, because they find more "signals". More trades means more fee drag, which is precisely the cost the backtest screenshots leave out. An AI bot that wins 55% of trades and fires 40 times a day still hands its edge to the fee schedule unless the per-trade cost is managed.

So evaluate an AI bot the same way as any bot: net of fees, on your venue, at your size. And since the bot cannot negotiate fees, the only levers left are the ones below: maker fills where the strategy allows, the right venue, and cashback on every fill.

3 ways to cut a bot's fee bill

The 3 levers are cashback on every fee, maker first execution, and the exchange's own discount ladder, and they stack.

First, fee cashback: services like Trade Reclaim return 30 to 50% of the trading fees an account generates across 11 exchanges, Binance, Bybit and OKX included. It works from the account's public UID, so it applies to API trading with zero integration: the bot does not know it exists, no code changes, no API key sharing, and the cashback arrives as USDT. It is the only lever that requires neither volume nor capital.

Second, execution style: every entry the strategy can plan should rest on the book as a maker order; on the major venues that alone cuts the futures fee per fill by half or more, and post only flags make it enforceable.

Third, the exchange ladder: VIP tiers and exchange token discounts lower the printed rate further, though they ask for volume or a token position in return. A bot running all three pays a fraction of the schedule its backtest probably assumed.

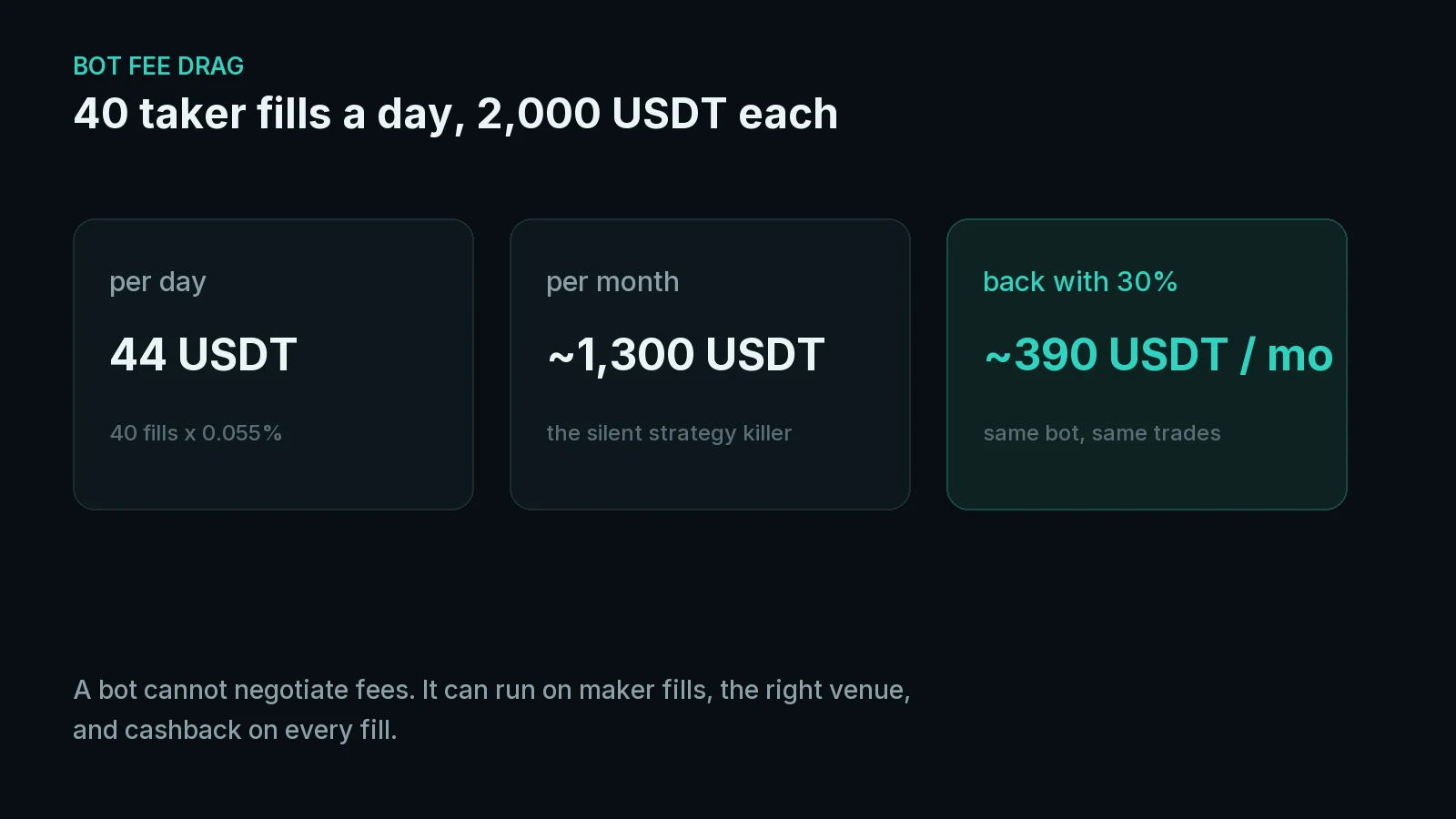

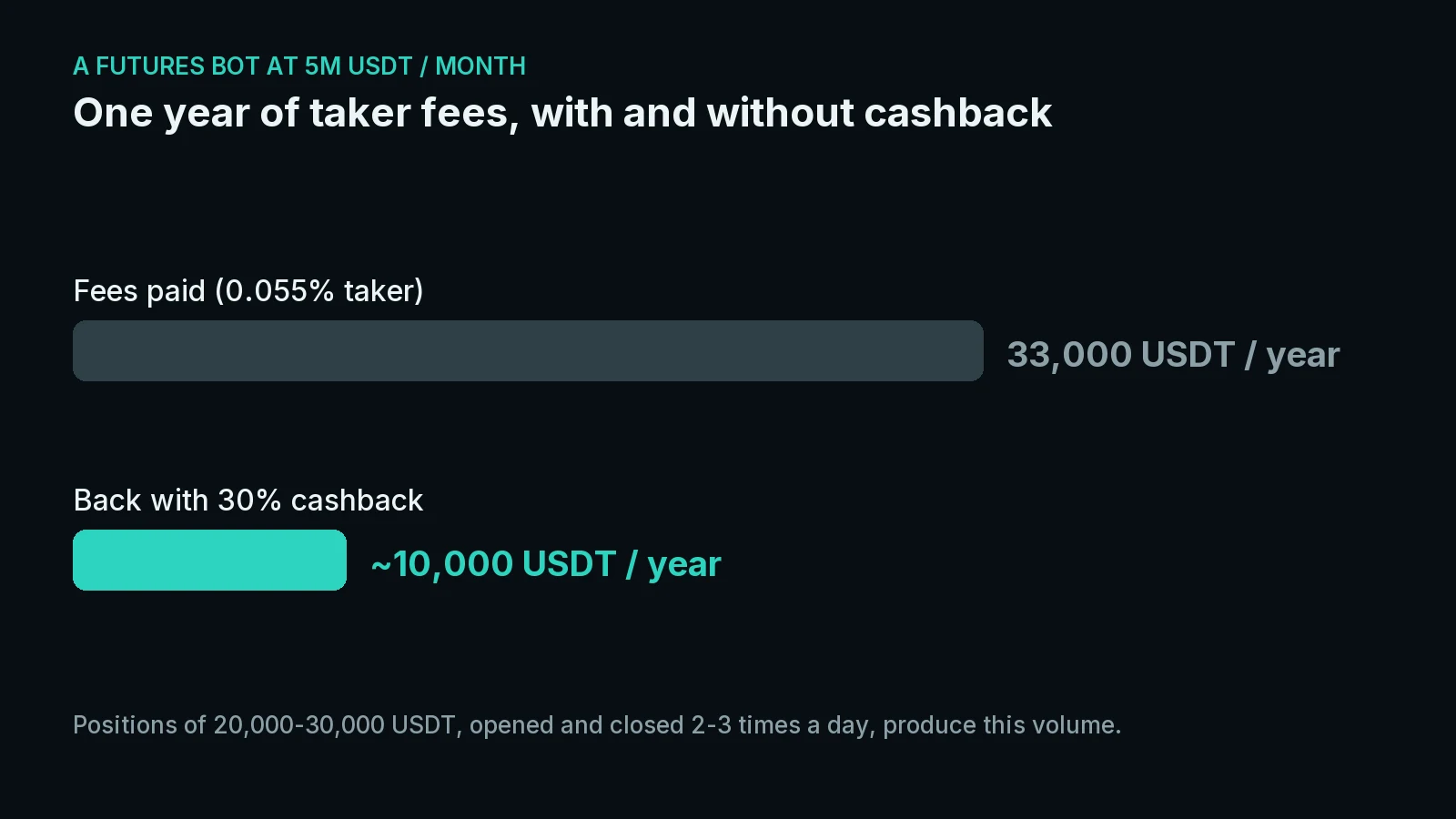

A worked example at real bot volume

A futures bot turning over 5 million USDT a month pays about 33,000 USDT a year in fees at standard taker rates, and gets roughly 10,000 of it back with cashback alone.

The volume is not exotic: positions of 20,000 to 30,000 USDT, opened and closed 2 to 3 times a day, produce it. At a 0.055% taker rate that is 2,750 USDT in fees every month. With 30% cashback, 825 USDT of that returns monthly, call it 9,900 a year, before the bot's execution is touched at all.

Shift half the fills to maker and the annual fee bill drops by another 11,000 or so. For a strategy whose yearly expectation was 20,000 USDT on paper, this is not optimization at the margins. It is the difference between running a profitable system and donating the edge to the fee schedule.

Run your bot's fee numbers

Put your bot's monthly volume into the calculator and see what its fees cost per year, and what 30 to 50% cashback returns. Then compare the effective rates across the 11 supported exchanges on one page.

Frequently asked questions

Do trading bots pay different fees than manual trading?

No. Orders sent over the API are charged the same maker and taker rates as manual orders on Binance, Bybit, OKX and the other major exchanges. There is no separate API fee schedule. Rate limits and request weights differ by exchange, but the cost per filled order is identical.

Does fee cashback work with API trading and bots?

Yes, fully. Cashback services like Trade Reclaim run on the exchange account's public UID and the volume the exchange reports against it. The bot needs no integration, no code changes and no shared API keys; every fee its orders generate earns the same 30 to 50% back as manual trades.

Are crypto trading bots profitable in 2026?

Some are, and fees are usually the deciding line. A bot is profitable when its average edge per trade exceeds its cost per trade; with taker round trips at 10 to 12 basis points and typical bot edges not much wider, the result is decided by execution style and effective fees as much as by the strategy itself.

Which exchange is best for running a trading bot?

The one where API reliability, order book depth and effective fees meet for your pair and size. Compare websocket stability and rate limits first, then real depth at your trade size, then the fee after VIP tier, token discount and cashback rather than the headline rate. That ranking differs by strategy, which is why the comparison is worth running with your own numbers.

Sofia Dani is Head of Marketing at Trade Reclaim, based in Switzerland. She earned a Bachelor of Arts at the University of Lucerne and went on to complete a Master's degree. She has little patience for products that win by confusing people, and covers crypto exchanges, their products, and what trading actually costs.

Trade Reclaim earns from exchange referrals and shares most of it back to you as cashback. Education, not financial advice.